Hospitals, Insurance & Biggest Risks In Thailand

Healthcare isn’t the most exciting topic when you’re thinking about moving to Thailand. But if you’re planning to live here long-term, it’s something you need to think about.

So today we’re going to talk about healthcare and health insurance here in the Kingdom. From the hospitals themselves and costs to the confusing and often frustrating world of insurance, coverage options, and your biggest risks.

And this is one of those topics where the details matter and expats can have very different experiences. So think of this as a guide, but also an invitation to share your own stories and any additional information because sometimes the best advice comes from conversations with other expats. And this definitely applies to healthcare.

Thailand’s Healthcare System: Public vs. Private

Thailand’s healthcare system is built on a public-private model and understanding that divide is essential before you even start thinking about insurance.

On one side are government hospitals. Everything from small provincial facilities to the country’s major research institutions in Bangkok such as Chulalongkorn. These are vast university-linked hospitals. The equipment is modern, the specialists are excellent, but public hospitals come with predictable tradeoffs. Wait times can be long, the process bureaucratic, and the level of English outside the elite teaching hospitals is often limited.

On the private side, you’ll find everything from nonprofit hospitals like St. Louis all the way up to luxury brands like Bangkok Hospital. At the top end, the hospitals generally resemble five-star hotels and are part of Thailand’s vast medical tourism industry. English is fluent, the staff is attentive, and appointments can often be booked the same day. The bills, of course, reflect that experience.

A routine checkup that might cost 400 baht in a public hospital can easily run 3 to 5,000 baht in a private one. A private room can cost 6 to 12,000 baht per night, while a hip replacement typically ranges between 250,000 and 500,000 baht (around 7 to 14,000 US dollars), depending on the hospital and materials used.

Conversely, surgeries at public hospitals will normally cost less than half that price, but even then, the expenses can add up quickly.

Overall, you have plenty of options in Thailand. But before you make the move, it’s essential to understand where you’ll actually go if and when you get sick, how quickly you’ll be seen, whether you can communicate effectively, and how you’ll pay. You want to figure all of this out in advance because if you’re faced with a significant injury or diagnosis, the last thing you’ll want to do is try to navigate a foreign healthcare system.

Thai Insurers vs. International Insurers

And perhaps the single most important decision you’ll need to make is choosing a health insurance plan. So let’s begin with two very different paths that you’ll encounter as soon as you start shopping.

Thai insurers on one side and international insurers on the other.

Thai insurers are popular because they’re generally cheaper and often have strong direct hospital billing networks. The most popular choices are Pacific Cross, Luma, AIA, and Krung Thai Axa. But Thai plans often come with strings attached. Coverage limits tend to be lower. Very few policies cover pre-existing conditions and age caps can be strict. For younger or mid-expats, Thai plans can work well, especially if you mostly use local hospitals. But for retirees, the group most likely to face serious illness, those renewal limits can become a deal breaker.

International insurers sit at the opposite end of the spectrum. These include major players like Allianz, Bupa, Cigna, and April International. Their premiums are steep, sometimes double or even triple the Thai plans. But in return, the benefits tend to be much broader with higher limits that can even be unlimited, lifetime renewals, and coverage outside Thailand, including medical evacuation. They’re much better designed for the nightmare scenarios: cancer treatment, major surgery or transplant, or emergency evacuation to Singapore.

The catch is the cost. By your 70s, international premiums can rival your rent, and the hospital networks generally only include the major hospitals. If you need to visit a smaller regional hospital, you may need to pay first and file a claim later, floating thousands of dollars until reimbursement comes through.

Ultimately, the right choice depends on your age, your health, and whether you plan to stay in Thailand full-time or keep traveling regionally.

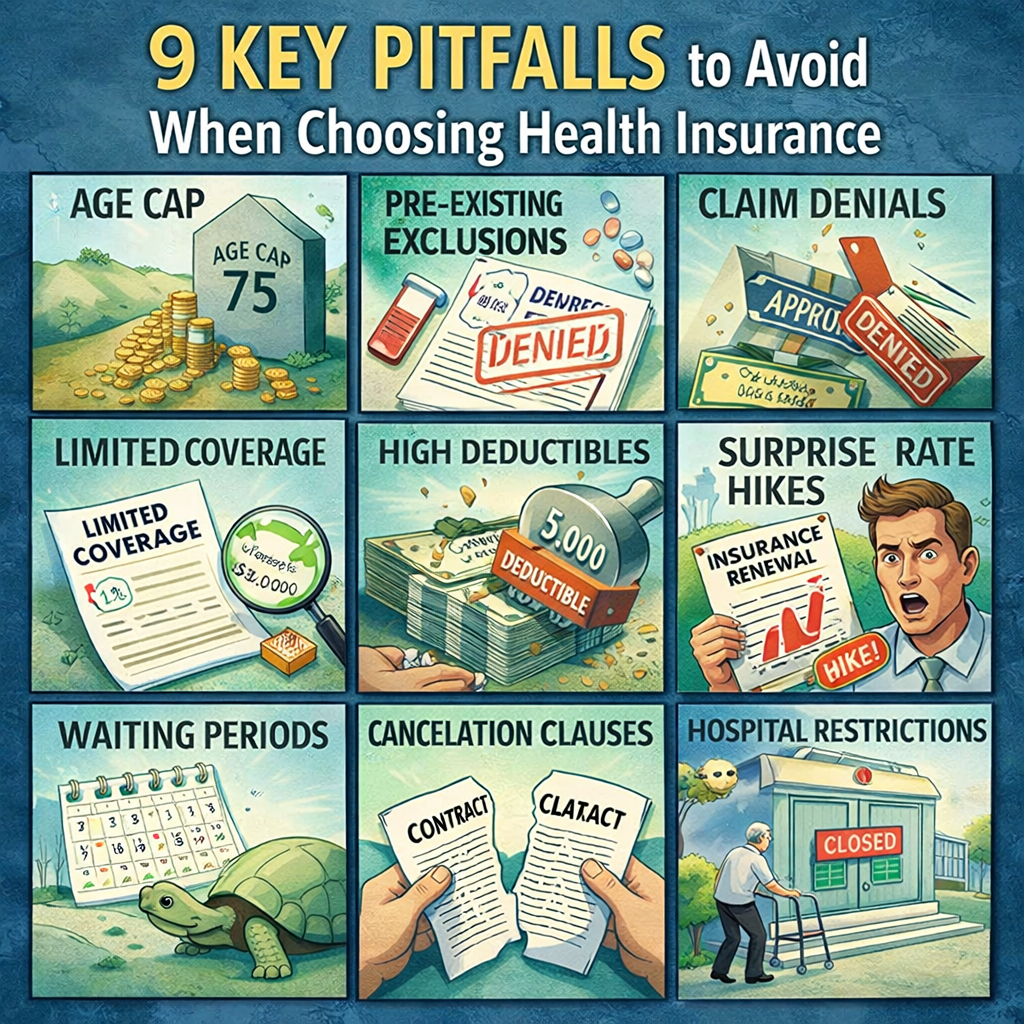

9 Key Pitfalls to Avoid When Choosing Health Insurance

But what about the specific policies, risks, and the fine print? On paper, a policy might look simple, but buried in the fine print are traps that can undo your coverage exactly when you need it most. And there are nine key pitfalls that you need to avoid when choosing an insurance policy.

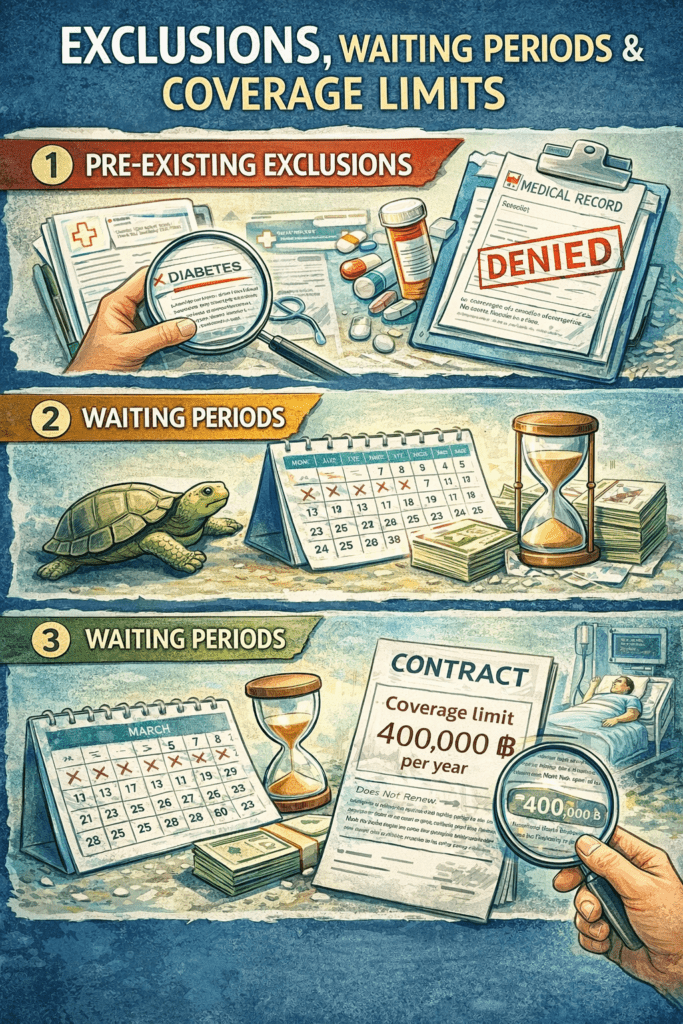

1. Renewal Age Caps

First, we have those renewal age caps that I mentioned already. This is a big one. Some Thai policies look fantastic until you realize they stop at 75. Others stop taking new clients at 70, but let existing ones renew a bit longer. And yes, a few rare policies renew for life, but you must buy early. And even then, exclusions can expand as you age. Imagine paying premiums faithfully for 15 years only to be dropped right when you need surgery. That’s why lifetime renewals matter.

2. Exclusions for Pre-Existing Conditions

Second are the exclusions. If you have diabetes, cancer, or even a minor flagged issue in your medical record, don’t assume it’s covered, especially with local policies which tend to exclude pre-existing conditions. But even international ones may write exclusions into the contract. Some use full medical underwriting, carving those conditions out forever, while others use moratorium underwriting, excluding them temporarily and then reassessing. Either way, if you don’t get those details clarified in writing, you may find yourself unprotected.

3. Waiting Periods

Third, check for waiting periods. Coverage doesn’t always start the day you sign. Most policies have 30 to 120 day waiting periods for illness protection, with only accidents covered from day one. Many expats learn this the hard way. They sign up, fall ill a month later, and discover their plan won’t pay yet.

4. Coverage Limits

Fourth, we’ve got coverage limits. And this is a mistake which can be caused by confusing retirement visa rules. If you apply for an OA retirement visa, Thai immigration stipulates that you need local coverage with inpatient insurance coverage up to 400,000 baht. While it satisfies the immigration rule, it does not offer much protection. If you opt for an OA visa, don’t make the mistake of assuming that this coverage is sufficient. Real protection means 3 to 5 million baht coverage per year at minimum. And you need to check whether the cap resets annually or is lifetime. You want the annual reset because a chronic illness can stretch over many years.

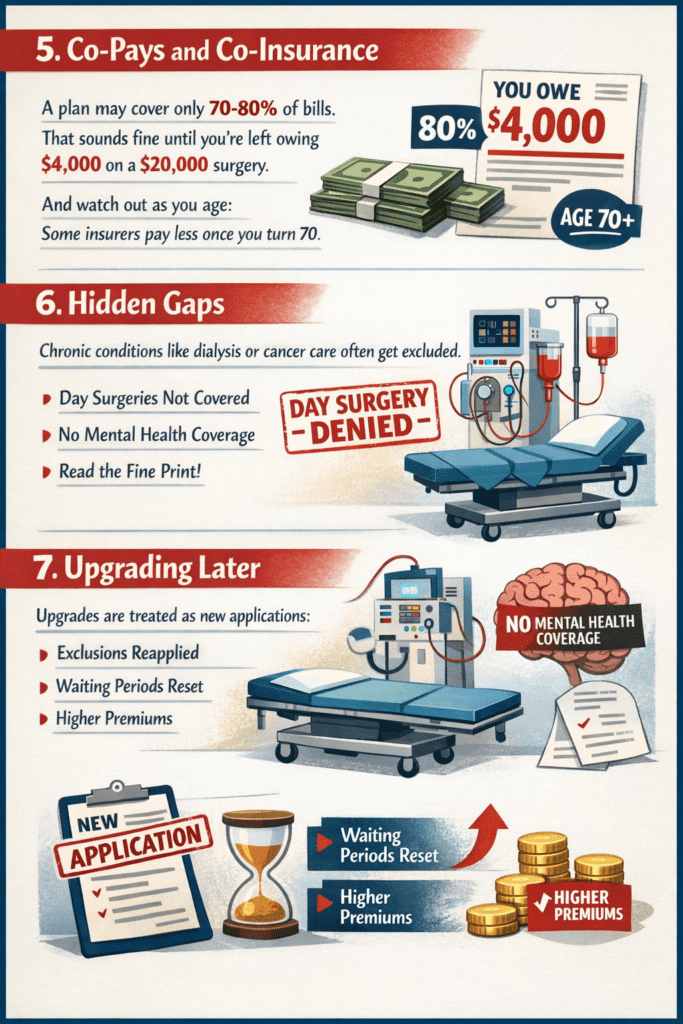

5. Co-Pays and Co-Insurance

Fifth are co-pays and co-insurance. A plan might look affordable upfront but cover only 70 or 80% of bills. That sounds fine until you’re left owing $4,000 on a $20,000 surgery. Worse, some local insurers introduce co-insurance clauses once you turn 70, paying only 80% or less and forcing you to self-insure the rest.

6. Hidden Gaps

Sixth, you need to check for hidden gaps. Many policies quietly exclude chronic conditions like dialysis, chemotherapy, or long-term cancer care. These long-tail expenses are the very things most likely to cause financial ruin. Yet, they’re precisely the ones many policies omit.

And the fine print can get tricky. For example, inpatient-only plans sometimes exclude day surgeries because you weren’t technically admitted. So a cataract procedure or colonoscopy done as a same-day case may not be reimbursed unless coded as inpatient.

Also pay attention to mental health coverage. Many policies, especially local ones, exclude psychiatric care, counseling, and medication altogether. It’s one of the most overlooked exclusions and one of the hardest to appeal.

7. Upgrading Later

Seventh is the risk of upgrading later. Some people assume they can start with a cheaper plan and upgrade later. But in practice, upgrades are normally treated as new applications, exclusions are reapplied, waiting periods reset, and premiums recalculated at your new age.

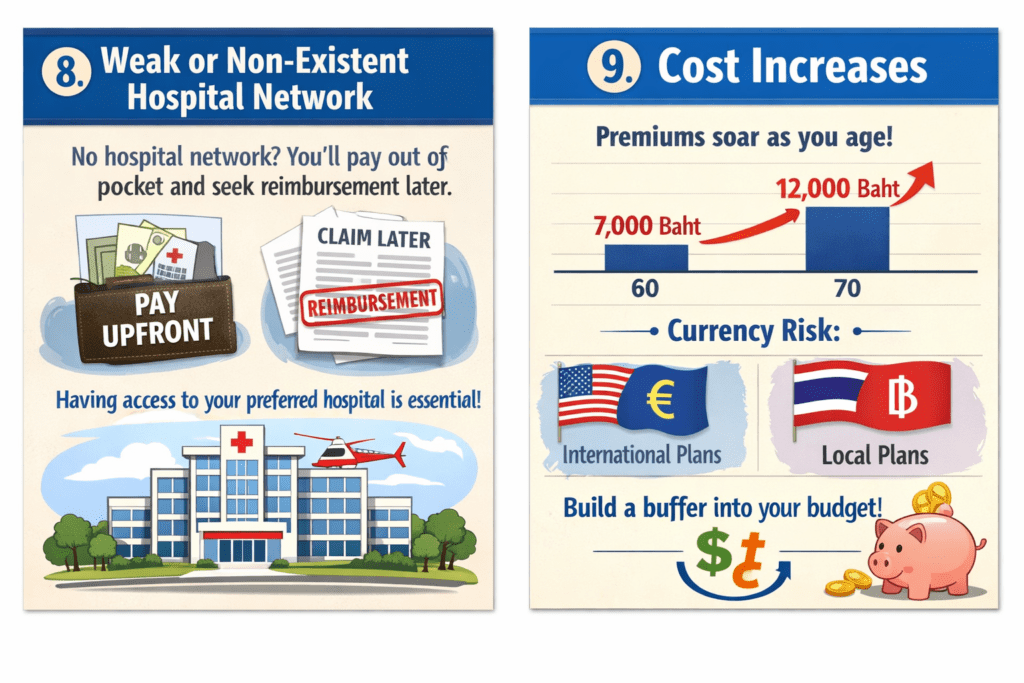

8. Weak or Non-Existent Hospital Network

At number eight is the weak or non-existent hospital network. Some plans may offer excellent rates and good coverage, but they lack a hospital network, and this means that you’ll need to pay out of pocket and then apply for reimbursement from the insurance provider. For long-term expats and retirees, a strong network that includes your preferred hospital is ideal.

9. Cost Increases

And finally, we have cost increases. At 60, a local plan might cost 5,000 to 7,000 baht per month, while an international plan may be 10,000 to 20,000. But once you hit 70, the numbers change dramatically, normally increasing by 50 to 75%. On average, premiums climb 10 to 15% every year as you get older, and you need to build that into your long-term budget.

Then there’s currency risk. International plans are priced in dollars or euros, while local plans are paid in baht. Both options present currency swing risks, and you need a reasonable buffer to protect yourself if you’re buying a plan that isn’t priced in your home currency.

How to Protect Yourself: Best Practices

So, what’s the best way to protect yourself when it comes to healthcare and health insurance?

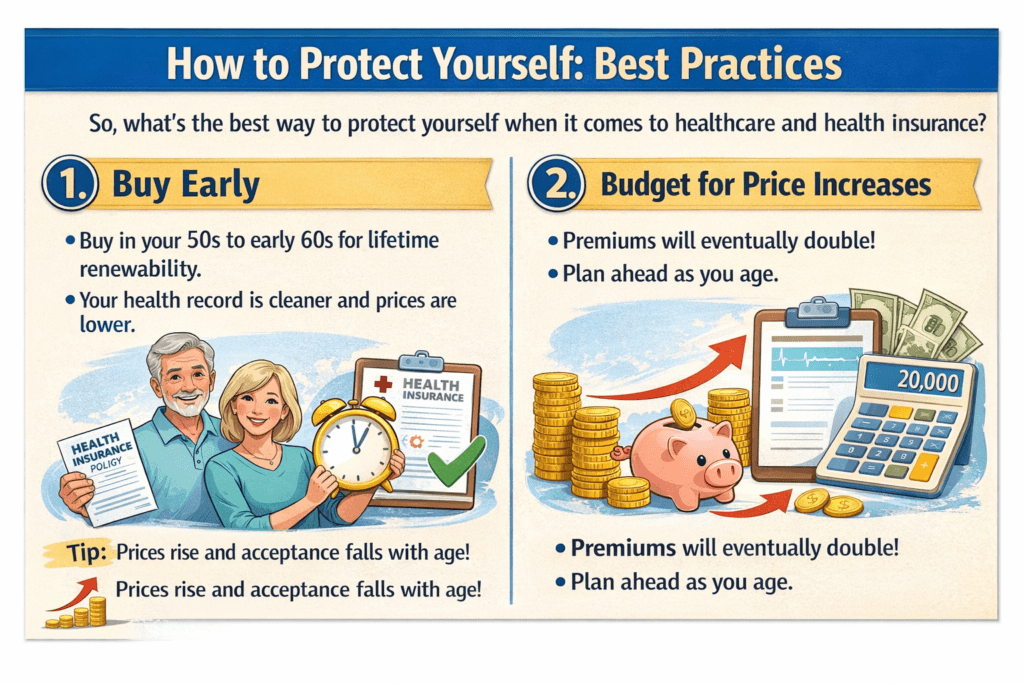

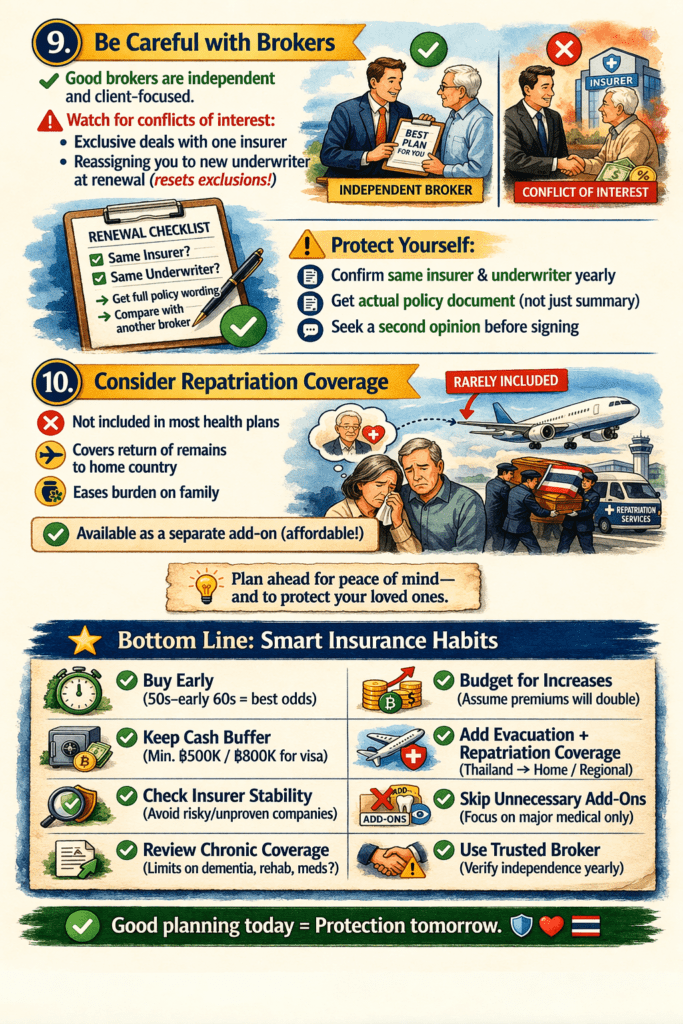

1. Buy Early

Buy early. If you buy insurance in your 50s or early 60s, you’re far more likely to be accepted and to secure lifetime renewability. Wait until 70 and the door may already be closed or the price will be beyond reach. And once you reach your late 60s, expect most insurers to require a full medical checkup. Even mild hypertension or high cholesterol can lead to exclusions. If you want the best odds of approval, apply while your medical record is still relatively clean.

2. Budget for Price Increases

Budget for price increases. Don’t assume your 10,000 baht premium at 60 will stay that way. Premiums rise, currencies fluctuate, and medical inflation doesn’t slow down. Assume that any plan will double within a decade, and plan accordingly.

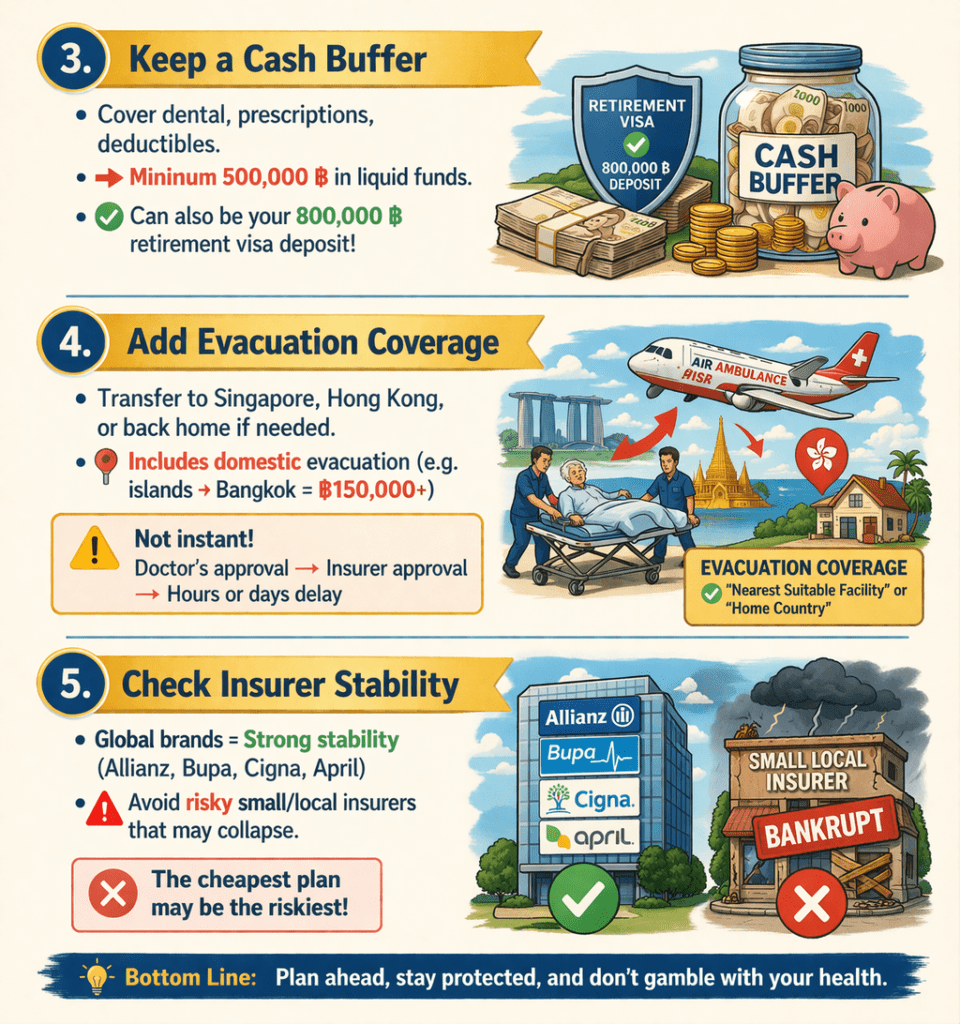

3. Keep a Cash Buffer

Keep a cash buffer. You’ll likely still need to pay out of pocket for dental care, prescriptions, and deductibles. Keep a minimum of 500,000 baht in liquid funds available. If you’re on a retirement visa, this can be the 800,000 baht bank deposit requirement.

4. Add Evacuation Coverage

Add evacuation coverage. Thailand’s hospitals are excellent, but no system is perfect. Evacuation benefits let you transfer to Singapore, Hong Kong, or even back home if needed. Some policies cover evacuation to the nearest suitable facility, others only to your home country. A small clause that can make a life-saving difference. And it’s not just about international evacuation. If you live on an island or remote province, make sure domestic air evacuation is also covered. A simple transfer to Bangkok can cost over 150,000 baht. And even with coverage, remember that evacuation isn’t instant. It usually requires a doctor’s certification and insurer pre-approval, which can take hours or even days.

5. Check Insurer Stability

Check insurer stability. A big international brand isn’t going anywhere, but smaller local insurers have folded or exited the market before. When they collapse, so does your coverage. The cheapest plan may be the riskiest.

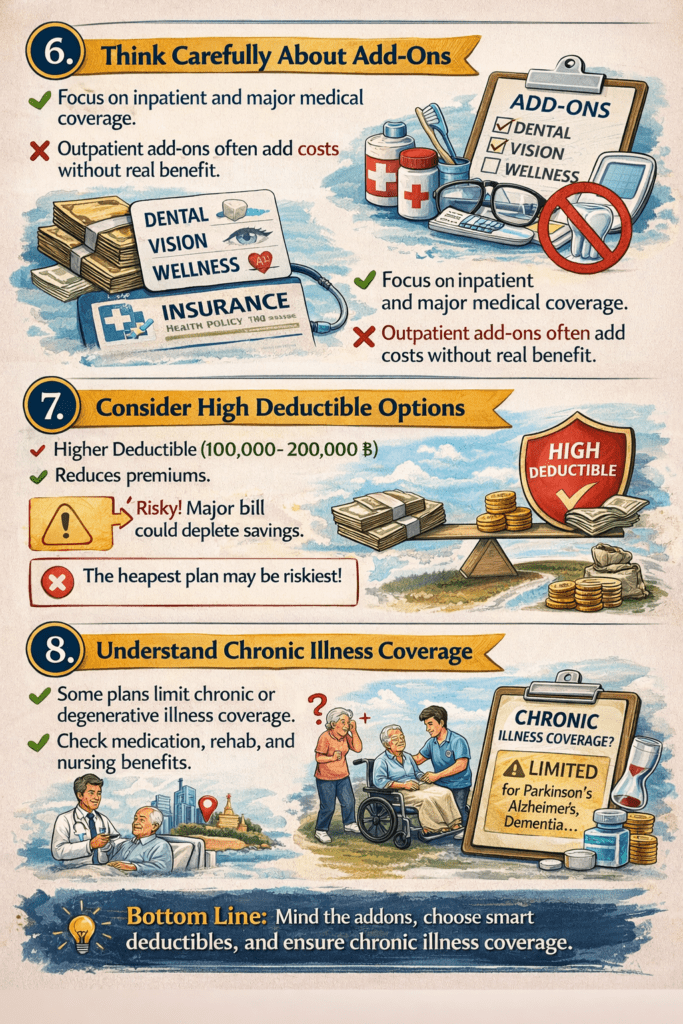

6. Think Carefully About Add-Ons

Think carefully about add-ons. Dental, vision, and wellness packages are tempting, but unless you’ll use them heavily, they add costs without meaningful protection. Focus on inpatient and major medical coverage the expenses that actually threaten your savings. Most outpatient services are fairly inexpensive and can be paid out of pocket.

7. Consider High Deductible Options

Here’s where some retirees are strategic. If you prefer, you can look into high deductible options. Some insurers will let you raise your deductible to 100,000 or 200,000 baht, which can cut monthly premiums dramatically. It’s risky, but it’s a way to keep lifetime coverage affordable as you age while paying for outpatient and smaller inpatient services out of pocket.

Others go a step further and self-insure, setting aside what they’d otherwise pay in premiums and using that money as an emergency fund. It’s a controversial approach and generally not recommended. One diagnosis or major accident can wipe out those savings, and you’ll find a few too many GoFundMe pages trying to raise money for hospital coverage when things go wrong.

8. Understand Chronic Illness Coverage

Another issue rarely discussed is chronic or degenerative illness. Some policies quietly limit coverage for long-term conditions like Parkinson’s, Alzheimer’s, or dementia, especially after age 70. Others restrict medication reimbursements to 12 months per diagnosis. Always check how your insurer defines “chronic.” That word alone can determine whether years of treatment are covered or not. You should also review what happens if you need long-term rehab or physical therapy. Some insurers exclude long-term physical therapy or home nursing entirely.

9. Be Careful with Brokers

And finally, when it comes to brokers, tread carefully. Good brokers are independent and will help you select an ideal policy that matches your needs, but some brokers work under exclusive contracts with specific insurers, and their commission depends on steering you towards certain plans. And some may even migrate their clients to a new underwriter during renewal, effectively resetting exclusions without notice.

If you use a broker, confirm each year that your renewal is with the same insurer and underwriter. Ask for a copy of the actual policy wording, not just the summary. And don’t hesitate to get a second opinion from another broker before signing.

10. Consider Repatriation Coverage

And finally, something few people talk about. Most policies don’t include repatriation of remains or funeral transport. That’s a separate coverage entirely and one that’s worth considering. Without it, the financial and logistical burden often falls on family members. Some hospitals or embassies can help arrange it, but it’s far easier and cheaper to plan ahead.

What Happens When You Visit a Thai Hospital

So, let’s talk about exactly what happens when you actually walk into a hospital here in Bangkok.

When you go to a Thai hospital, even with an appointment, bring your passport. You’ll need it for registration. The process can take a while the first time and it can be best to pre-register at your preferred hospital to avoid any delays in emergency situations.

And it’s best to ensure that the hospital has direct billing, even if it’s technically part of your hospital network. Miscommunication between the billing department and your insurer can leave you stuck paying out of pocket until the paperwork clears.

Normally, you can see a specialist directly without any significant wait times. Thai insurers don’t require referrals for a claim, but some international insurers do. If your plan follows Western-style referral systems, you might need a GP letter or pre-authorization before the visit, otherwise reimbursement could be denied on a technicality. Always check the fine print and confirm ahead of time.

When you see the doctor, the attention and service is generally excellent, but you need to watch out for overprescription and upselling. You’ll often be offered additional blood tests, scans, or branded medications that might not be strictly necessary. The doctors are very competent, but they work within a private enterprise.

If a service or treatment is recommended, always ask if it’s essential. And make sure to request generic medications or request the prescription directly and buy them at an offsite pharmacy.

Most medications are available over the counter in Thailand, but opioids and opioid derivatives are strictly controlled. You’ll need special permission from the Thai FDA to bring an opioid medication and a prescription from a Thai doctor at a large hospital for longer-term access.

If you require follow-up care, make sure to schedule the appointment. Thailand excels in acute treatment surgeries, diagnostics, emergency response but continuity of care can be inconsistent. Once the procedure is done, discharges can be fast, and long-term rehabilitation or physical therapy may not be emphasized. It’s normally up to you to book a follow-up appointment.

Depending on your insurance coverage, you may also want to ask the doctor if they have any work at a public hospital. Most doctors split time between the top-tier private hospitals and big research hospitals. And if you require longer-term care, they may be able to book you in for follow-up care at the public hospital at a much lower cost.

And always remember, paperwork matters. If you ever have a claim that’s rejected for an unclear reason, check the diagnosis code. Thai hospitals sometimes use localized ICD10 coding that doesn’t perfectly match what your insurer’s software expects. A small translation mismatch is all it takes to trigger an automated denial.

If you file your own claim, make sure every page is stamped and signed by a Thai licensed physician, ideally in Thai. Some insurers insist on Thai language documentation. And missing a doctor’s stamp can be enough for a claim to bounce.

Executive Health Checkups and Emergency Numbers

One of the best hidden values in Thailand’s healthcare system is the executive health checkup. These are full body screenings: blood work, imaging, cardiac testing, cancer screenings, and specialist consultations. Many expats do one every year or two. It’s proactive healthcare that can catch problems early before they turn into expensive emergencies.

And if you ever face a medical emergency in Thailand, the nationwide ambulance number is 1669 or 1646 if you’re in Bangkok. Or if you pre-register with a hospital, you can normally use their dedicated ambulance service number.

The big private hospitals generally provide streamlined service in English, but outside the major cities and tourist hotspots, this quickly drops off. Many provincial hospitals rely on translation apps or relatives to interpret. You may need to access these hospitals on holiday, and it’s wise to keep a printed summary of your allergies, medications, and insurance information in Thai so doctors have something clear to reference in case of an emergency.

Final Advice: How to Choose the Right Policy

So, here’s the truth. Health insurance in Thailand is sometimes complicated, frustrating, and expensive, but it’s absolutely essential. Without it, one accident or diagnosis can undo your entire retirement plan.

You have plenty of insurers and potential policies to choose from, and you now have the tools to decide on the best one. But what next?

Well, first of all, check discussion forums like Reddit or ideally the comment section of a video like this. Stories from fellow expats and retirees that are in a similar situation can be the most helpful guidance, especially from those who’ve actually used their coverage.

Use the forums and guidance to make an initial list or start with the providers I covered here and get a quote from each company. Read the fine print. Look out for the nine key pitfalls I covered. Pay attention to things like waiting periods, hospital networks, and renewal age limits.

Once a policy looks interesting and you’ve checked the fine print closely, get back to those forums. Ask plenty of questions about the specific policy, see if you can find fellow expats or retirees who can share their experiences. The more feedback you get, the better.

This shouldn’t be a rushed decision, especially for retirees. You’re choosing a policy that should be with you for the next decade or two. It’s a huge investment decision. Take your time. It might be annoying, but it’s worth the effort.